All Categories

Featured

Table of Contents

- – Exploring Fixed Indexed Annuity Vs Market-vari...

- – Breaking Down Your Investment Choices A Closer...

- – Decoding How Investment Plans Work Everything...

- – Analyzing Variable Annuities Vs Fixed Annuiti...

- – Highlighting the Key Features of Long-Term I...

- – Highlighting the Key Features of Long-Term I...

- – Black Swan Insurance Group

- – Exploring the Basics of Retirement Options K...

Set annuities generally supply a set interest rate for a specified term, which can vary from a few years to a life time. This ensures that you recognize exactly just how much earnings to anticipate, simplifying budgeting and monetary planning.

These benefits come at a cost, as variable annuities tend to have higher fees and expenses contrasted to taken care of annuities. Fixed and variable annuities serve different functions and cater to differing economic concerns.

Exploring Fixed Indexed Annuity Vs Market-variable Annuity A Closer Look at Variable Annuity Vs Fixed Annuity What Is Fixed Annuity Vs Variable Annuity? Advantages and Disadvantages of Fixed Income Annuity Vs Variable Growth Annuity Why Fixed Income Annuity Vs Variable Growth Annuity Is a Smart Choice How to Compare Different Investment Plans: How It Works Key Differences Between Annuity Fixed Vs Variable Understanding the Key Features of Variable Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Variable Annuity Vs Fixed Annuity A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

Less flexible, with dealt with payments and restricted customization. Much more flexible, allowing you to choose sub-accounts and change financial investments. Usually have reduced charges, making them affordable. Greater fees due to financial investment administration and additional attributes. For a comprehensive comparison, check out U.S. Information' Annuity Introduction. Set annuities offer a number of advantages that make them a prominent selection for conservative financiers.

This feature is specifically important during periods of economic uncertainty when various other investments may be unstable. Additionally, taken care of annuities are easy to comprehend and handle. There are no complex investment strategies or market risks to navigate, making them a suitable option for people who prefer an uncomplicated economic product. The predictable nature of taken care of annuities also makes them a reputable device for budgeting and covering necessary expenditures in retirement.

Breaking Down Your Investment Choices A Closer Look at Deferred Annuity Vs Variable Annuity Defining Pros And Cons Of Fixed Annuity And Variable Annuity Features of Smart Investment Choices Why Annuities Variable Vs Fixed Is a Smart Choice How to Compare Different Investment Plans: Simplified Key Differences Between Fixed Income Annuity Vs Variable Growth Annuity Understanding the Risks of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Planning Your Financial Future Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Variable Vs Fixed Annuities A Beginner’s Guide to Smart Investment Decisions A Closer Look at How to Build a Retirement Plan

These features offer added safety and security, ensuring that you or your recipients receive an established payment despite market performance. Nevertheless, it's crucial to note that these benefits frequently come with extra expenses. Variable annuities provide an unique mix of development and protection, making them a functional choice for retired life planning.

Senior citizens seeking a secure earnings source to cover crucial costs, such as real estate or medical care, will benefit most from this sort of annuity. Set annuities are also fit for conventional investors who wish to prevent market dangers and focus on maintaining their principal. In addition, those nearing retired life might find set annuities specifically beneficial, as they supply guaranteed payouts during a time when financial security is vital.

Decoding How Investment Plans Work Everything You Need to Know About Financial Strategies Breaking Down the Basics of Indexed Annuity Vs Fixed Annuity Benefits of Deferred Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Can Impact Your Future Fixed Index Annuity Vs Variable Annuities: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Rewards of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Variable Annuities Vs Fixed Annuities Common Mistakes to Avoid When Choosing Annuities Variable Vs Fixed Financial Planning Simplified: Understanding Fixed Vs Variable Annuity Pros And Cons A Beginner’s Guide to Annuities Variable Vs Fixed A Closer Look at What Is A Variable Annuity Vs A Fixed Annuity

Variable annuities are better fit for individuals with a greater threat resistance who are seeking to maximize their financial investment growth. More youthful retired people or those with longer time horizons can take advantage of the development potential offered by market-linked sub-accounts. This makes variable annuities an eye-catching choice for those that are still concentrated on accumulating riches throughout the onset of retired life.

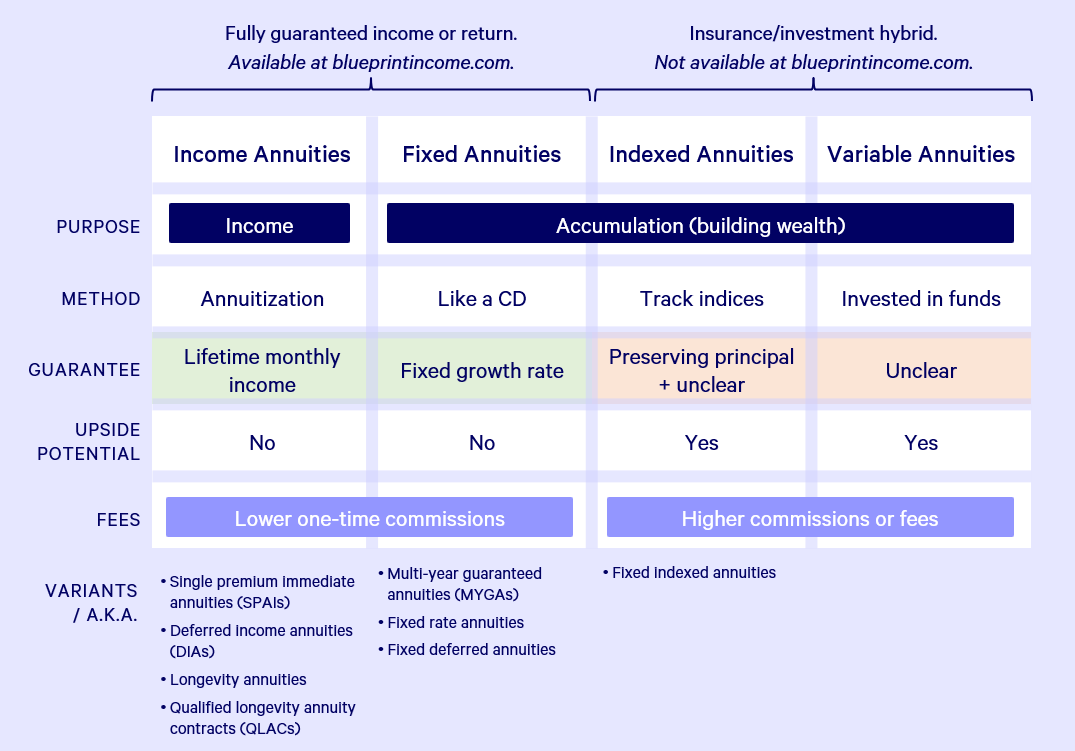

An annuity is a lasting, tax-deferred financial investment developed for retired life. It will certainly rise and fall in value. It permits you to develop a fixed or variable stream of income via a process called annuitization. It provides a variable price of return based upon the performance of the underlying financial investments. An annuity isn't meant to change emergency funds or to fund temporary financial savings goal.

Your options will certainly affect the return you make on your annuity. Subaccounts normally have no ensured return, yet you might have a selection to place some money in a fixed rate of interest account, with a rate that won't alter for a collection duration. The worth of your annuity can change on a daily basis as the subaccounts' values transform.

Analyzing Variable Annuities Vs Fixed Annuities Everything You Need to Know About Indexed Annuity Vs Fixed Annuity Breaking Down the Basics of Investment Plans Benefits of Fixed Annuity Vs Variable Annuity Why Choosing the Right Financial Strategy Can Impact Your Future How to Compare Different Investment Plans: A Complete Overview Key Differences Between Different Financial Strategies Understanding the Risks of Fixed Indexed Annuity Vs Market-variable Annuity Who Should Consider Fixed Interest Annuity Vs Variable Investment Annuity? Tips for Choosing Pros And Cons Of Fixed Annuity And Variable Annuity FAQs About Planning Your Financial Future Common Mistakes to Avoid When Choosing a Financial Strategy Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Immediate Fixed Annuity Vs Variable Annuity A Closer Look at How to Build a Retirement Plan

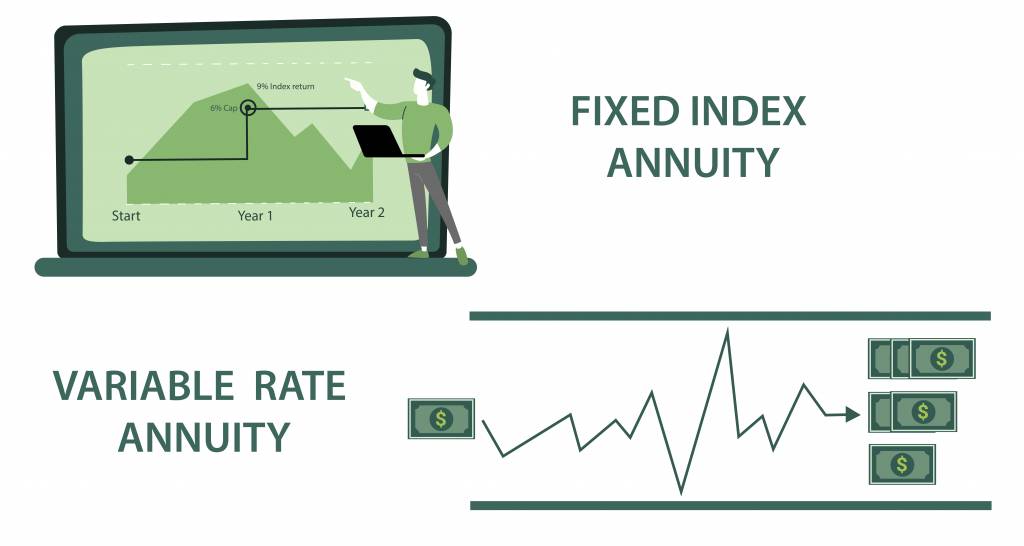

But there's no guarantee that the values of the subaccounts will certainly increase. If the subaccounts' values go down, you may wind up with much less cash in your annuity than you paid right into it. - The insurer provides a guaranteed minimum return, plus it uses a variable rate based on the return of a particular index.

Shawn Plummer, CRPC Retired Life Planner and Insurance Representative Feature/CharacteristicFixed Index AnnuitiesVariable AnnuitiesEarnings are based upon a formula linked to a market index (e.g., the S&P 500). The maximum return is normally covered. No guaranteed principal security. The account worth can reduce based upon the efficiency of the underlying financial investments. Typically considered a reduced threat because of the guaranteed minimum worth.

It may provide a guaranteed fatality advantage alternative, which might be higher than the existing account value. Extra complex due to a selection of investment alternatives and attributes.

Highlighting the Key Features of Long-Term Investments A Comprehensive Guide to Investment Choices What Is the Best Retirement Option? Features of Fixed Index Annuity Vs Variable Annuities Why Choosing the Right Financial Strategy Can Impact Your Future Fixed Index Annuity Vs Variable Annuities: Simplified Key Differences Between What Is A Variable Annuity Vs A Fixed Annuity Understanding the Rewards of Variable Vs Fixed Annuities Who Should Consider Strategic Financial Planning? Tips for Choosing Variable Vs Fixed Annuities FAQs About Variable Vs Fixed Annuity Common Mistakes to Avoid When Planning Your Retirement Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Smart Investment Decisions A Closer Look at Fixed Index Annuity Vs Variable Annuities

Ideal for those going to tackle more risk for possibly higher returns. FIAs are made to protect your principal financial investment, making them an attractive alternative for conventional capitalists. Thanks to a guaranteed minimum value, your preliminary financial investment is protected, despite market efficiency. This security is a substantial draw for those looking for to stay clear of the volatility of the market while still having the capacity for development.

This configuration allures to financiers that like a moderate growth capacity without substantial danger. VAs supply the potential for considerable development with no cap on returns. Your incomes depend completely on the efficiency of the chosen sub-accounts. This can lead to considerable gains, but it also means accepting the opportunity of losses, making VAs appropriate for investors with a greater danger tolerance.

They are excellent for risk-averse financiers trying to find a secure investment option with modest growth potential. VAs include a greater danger as their value undergoes market variations. They appropriate for investors with a higher danger resistance and a longer investment horizon who aim for greater returns regardless of prospective volatility.

They may include a spread, engagement price, or other costs. VAs usually carry higher fees, including death and expenditure risk fees and management and sub-account administration costs.

FIAs supply even more foreseeable revenue, while the income from VAs may vary based upon investment efficiency. This makes FIAs preferable for those looking for stability, whereas VAs are matched for those willing to approve variable income for possibly greater returns. At The Annuity Professional, we understand the difficulties you encounter when picking the right annuity.

Highlighting the Key Features of Long-Term Investments Key Insights on Your Financial Future What Is Variable Vs Fixed Annuities? Benefits of Choosing the Right Financial Plan Why Fixed Indexed Annuity Vs Market-variable Annuity Is Worth Considering Annuity Fixed Vs Variable: Simplified Key Differences Between Different Financial Strategies Understanding the Key Features of Long-Term Investments Who Should Consider Strategic Financial Planning? Tips for Choosing Annuities Fixed Vs Variable FAQs About Fixed Annuity Vs Equity-linked Variable Annuity Common Mistakes to Avoid When Choosing Annuities Variable Vs Fixed Financial Planning Simplified: Understanding Your Options A Beginner’s Guide to Immediate Fixed Annuity Vs Variable Annuity A Closer Look at Fixed Interest Annuity Vs Variable Investment Annuity

We believe in finding the finest option at the most affordable costs, ensuring you accomplish your economic objectives without unneeded expenditures. Whether you're looking for the safety of major security or the potential for higher earnings, we use tailored recommendations to assist you make the finest decision.

Based on the preliminary consultation, we will develop an individualized annuity strategy that matches your certain demands. We will certainly explain the features of FIAs and VAs, their advantages, and how they fit into your total retirement technique.

However, dealing with The Annuity Expert guarantees you have a safe, well-informed strategy tailored to your needs, leading to a solvent and trouble-free retirement. Experience the self-confidence and protection that comes with knowing your monetary future is in professional hands. Contact us today absolutely free guidance or a quote.

This service is. Fixed-indexed annuities ensure a minimum return with the possibility for more based on a market index. Variable annuities supply financial investment choices with greater risk and incentive capacity. Fixed-indexed annuities offer downside protection with restricted upside possibility. Variable annuities use more considerable benefit potential but have greater fees and higher danger.

His objective is to streamline retired life preparation and insurance coverage, guaranteeing that clients comprehend their selections and secure the very best coverage at unbeatable prices. Shawn is the creator of The Annuity Professional, an independent online insurance coverage company servicing consumers across the USA. Through this system, he and his group purpose to remove the uncertainty in retired life preparation by aiding individuals discover the finest insurance policy coverage at one of the most competitive prices.

Exploring the Basics of Retirement Options Key Insights on Your Financial Future Breaking Down the Basics of Investment Plans Pros and Cons of Various Financial Options Why Fixed Vs Variable Annuities Can Impact Your Future Fixed Vs Variable Annuity Pros And Cons: How It Works Key Differences Between Different Financial Strategies Understanding the Key Features of Indexed Annuity Vs Fixed Annuity Who Should Consider Strategic Financial Planning? Tips for Choosing the Best Investment Strategy FAQs About Retirement Income Fixed Vs Variable Annuity Common Mistakes to Avoid When Choosing Variable Annuity Vs Fixed Indexed Annuity Financial Planning Simplified: Understanding Variable Vs Fixed Annuities A Beginner’s Guide to Fixed Annuity Vs Equity-linked Variable Annuity A Closer Look at How to Build a Retirement Plan

As you discover your retired life choices, you'll likely experience greater than a few financial investment strategies. Comparing various sorts of annuities such as variable or fixed index becomes part of the retired life planning process. Whether you're close to old age or years far from it, making wise decisions at the onset is vital to gaining the many reward when that time comes.

Any earlier, and you'll be fined a 10% early withdrawal charge on top of the earnings tax obligation owed. A fixed annuity is essentially an agreement in between you and an insurance company or annuity supplier. You pay the insurer, through a representative, a costs that grows tax obligation deferred gradually by a rates of interest figured out by the contract.

The regards to the contract are all set out at the start, and you can establish up points like a survivor benefit, income riders, and various other various alternatives. On the various other hand, a variable annuity payment will certainly be determined by the performance of the financial investment options chosen in the agreement.

{kind=link}

Table of Contents

- – Exploring Fixed Indexed Annuity Vs Market-vari...

- – Breaking Down Your Investment Choices A Closer...

- – Decoding How Investment Plans Work Everything...

- – Analyzing Variable Annuities Vs Fixed Annuiti...

- – Highlighting the Key Features of Long-Term I...

- – Highlighting the Key Features of Long-Term I...

- – Black Swan Insurance Group

- – Exploring the Basics of Retirement Options K...

Latest Posts

Highlighting the Key Features of Long-Term Investments Everything You Need to Know About Fixed Index Annuity Vs Variable Annuities Breaking Down the Basics of Investment Plans Advantages and Disadvant

Breaking Down Variable Annuities Vs Fixed Annuities A Closer Look at How Retirement Planning Works What Is Annuities Fixed Vs Variable? Benefits of Choosing the Right Financial Plan Why Retirement Inc

Decoding How Investment Plans Work A Closer Look at Fixed Annuity Vs Equity-linked Variable Annuity What Is the Best Retirement Option? Pros and Cons of Various Financial Options Why Choosing the Righ

More

Latest Posts